Higher materials prices are weighing heavily on single family construction

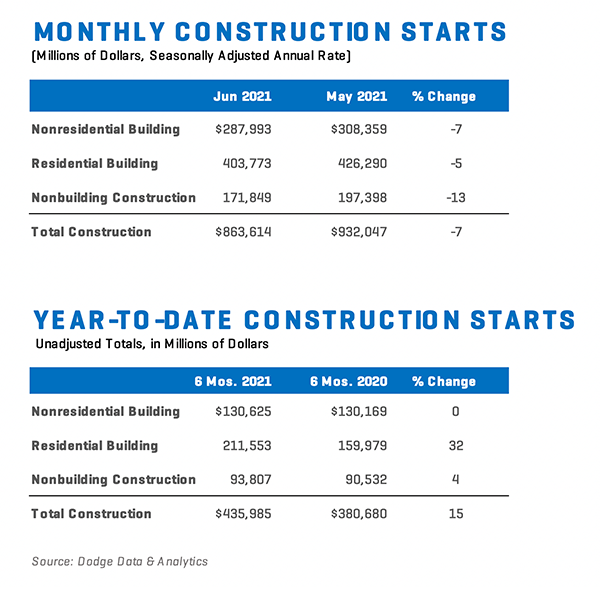

Total construction starts lost 7% in June, slipping to a seasonally adjusted annual rate of $863.6 billion, according to Dodge Data & Analytics. All three major sectors (residential, nonresidential building, and nonbuilding) pulled back during the month. Single family housing starts are feeling the detrimental effects of rising materials prices. Large projects that broke ground in May were absent in June for nonresidential building and nonbuilding starts, resulting in declines.

“Unabated materials price inflation has driven a significant deceleration in single family construction,” stated Richard Branch, Chief Economist for Dodge Data & Analytics. “Lumber futures have eased in recent weeks, but builders are unlikely to see much relief over the short-term, meaning building costs will continue to negatively influence the housing industry. On the other hand, the nascent recovery in nonresidential buildings has continued on as projects pile up in the planning stages. These mixed signals coming from both residential and nonresidential construction starts suggest that recovery from the pandemic will remain uneven in coming months as rising materials prices and labor shortages weigh on the industry.”

Below is the full breakdown:

- Nonbuilding construction starts lost 13% in June, dipping to a seasonally adjusted annual rate of $171.8 billion. While highway and bridge starts slid 7%, the overall decline in nonbuilding starts was the result of a 63% drop in the utility and gas plant category that followed a large increase in May. Total nonbuilding starts, excluding the utility/gas plant category, rose 3% on gains in environmental public works and miscellaneous nonbuilding. Total nonbuilding starts were up 4% within the first six months of 2021. Environmental public works surged 35%, while utility/gas plants gained 13%. Miscellaneous nonbuilding (-6%) and highway and bridge starts (-9%), however, dragged on the sector.

For the 12 months ending June 2021, total nonbuilding starts were 6% lower than the 12 months ending June 2020. Environmental public works starts were 23% higher, while utility and gas plant starts were down 20%. Highway and bridge starts were down 3% and miscellaneous nonbuilding starts were 22% lower through the first six months.

The largest nonbuilding projects to break ground in June were a $453 million sewer overflow project in Pawtucket RI, the $439 million Bay Park Conveyance Project in Cedar Creek NY, and the $390 million I-5 North Capacity Enhancement project in Los Angeles CA.

- Nonresidential building starts dropped 7% in June to a seasonally adjusted annual rate of $288.0 billion. Large healthcare and manufacturing projects provided a significant boost to May, but the absence of similar projects in June led to normalized starts activity. Without the negative influence of these sectors, nonresidential starts would have increased 10% in June. Commercial starts rose 12% with all categories posting gains, while institutional starts fell by 9% and manufacturing starts lost 62% over the month. Through the first six months of 2021, nonresidential building starts were slightly ahead of the first six months of 2020. Commercial starts were up 7% and manufacturing starts were 36% higher, while institutional starts were 5% lower through the first six months.

For the 12 months ending June 2021, nonresidential building starts were 14% lower than the 12 months ending June 2020. Commercial starts were down 18%, while institutional starts fell 10%. Manufacturing starts dropped 42% in the 12 months ending June 2021.

The largest nonresidential building projects to break ground in June were the $1.0 billion Research and Development District office project in San Diego CA, the $470 million second phase of the Oyster Point Offices in San Francisco CA, and the $410 million Amazon distribution center in Rochester NY.

- Residential building starts fell 5% in June to a seasonally adjusted annual rate of $403.8 billion. Single family starts lost 8%, while multifamily starts were 2% higher. From January through June, total residential starts were 32% higher than the same period a year earlier. Single family starts were up 37%, while multifamily starts were 19% higher.

For the 12 months ending June 2021, total residential starts were 22% higher than the 12 months ending June 2020. Single family starts gained 29%, while multifamily starts were up 5% on a 12-month sum basis.

The largest multifamily structures to break ground in June were the $400 million Courthouse Commons project in San Diego CA, the $267 million 1900 Crystal Ave residences in Arlington VA, and the $250 million Five Park Condominiums and Apartments in Miami Beach FL.

- Regionally, June’s starts rose in the Northeast but fell in all other regions.

Dodge Data & Analytics is North America’s leading provider of commercial construction project data, market forecasting & analytics services and workflow integration solutions for the construction industry. Building product manufacturers, architects, engineers, contractors, and service providers leverage Dodge to identify and pursue unseen growth opportunities that help them grow their business. On a local, regional or national level, Dodge empowers its customers to better understand their markets, uncover key relationships, seize growth opportunities, and pursue specific sales opportunities with success. The company’s construction project information is the most comprehensive and verified in the industry.

As of April 15th, Dodge Data & Analytics and The Blue Book — the largest, most active network in the U.S. commercial construction industry — combined their businesses in a merger. The Blue Book Network delivers three unparalleled databases of companies, projects, and people.

Dodge and The Blue Book offer 10+ billion data elements and 14+ million project and document searches. Together, they provide a unified approach for new business generation, business planning, research, and marketing services users can leverage to find the best partners to complete projects and to engage with customers and prospects to promote projects, products, and services. To learn more, visit: construction.com and thebluebook.com.

Last modified: July 26, 2021